How the invisible weight of running a medical practice is breaking doctors, and three startups quietly fixing it from the inside.

It is 7:42 AM. Before Dr. Reyes sees her first patient of the day, she has already spent 38 minutes dealing with a backlog of faxes that arrived overnight. Not letters. Not urgent alerts. Faxes, 47 of them. Lab results that require her signature. A referral request from a specialist that was supposed to go to a different physician. A hospital discharge summary for a patient who had emergency surgery three days ago and is now, apparently, back on her panel without anyone telling her.

Somewhere in that stack is the information that would change how she manages a diabetic patient she is seeing at 9 AM. But the discharge summary arrived as page 4 of a 12 page fax bundle, formatted for a printer, sent to a shared inbox that four physicians all use. She may catch it. She may not.

This is not a crisis. This is a Tuesday.

The administrative burden facing clinical medicine is well documented. But what gets lost in the data is what it actually feels like to run a practice. It is not dramatic. It is not a single breaking point. It is a thousand small friction moments that compound across the day, across the week, across a career — until the physician sitting across from a patient is physically present but cognitively already three tasks behind.

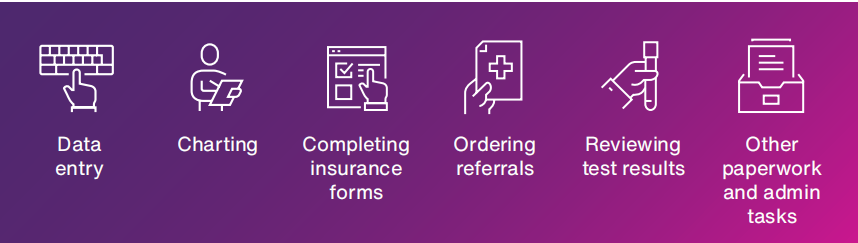

Administrative burden defined

Administrative burden refers to tasks and responsibilities that take time and energy away from patient care. These include:

The Volume Problem Nobody Warned Them About

According to TELUS Health’s Artificial Intelligence and the Future of Healthcare report, clinics using the TELUS Collaborative Health Record received 4.5 million faxes in 2023 alone, every one of which required a human to triage it.¹ These are not medical decisions. They are sorting tasks. And they are being performed by some of the most expensively trained people in the country.

Chris LeBouthillier, Executive Director at West Carleton Family Health Team, puts it plainly in the same report: *”The volume of information that comes into primary care is one of its biggest challenges.”*¹

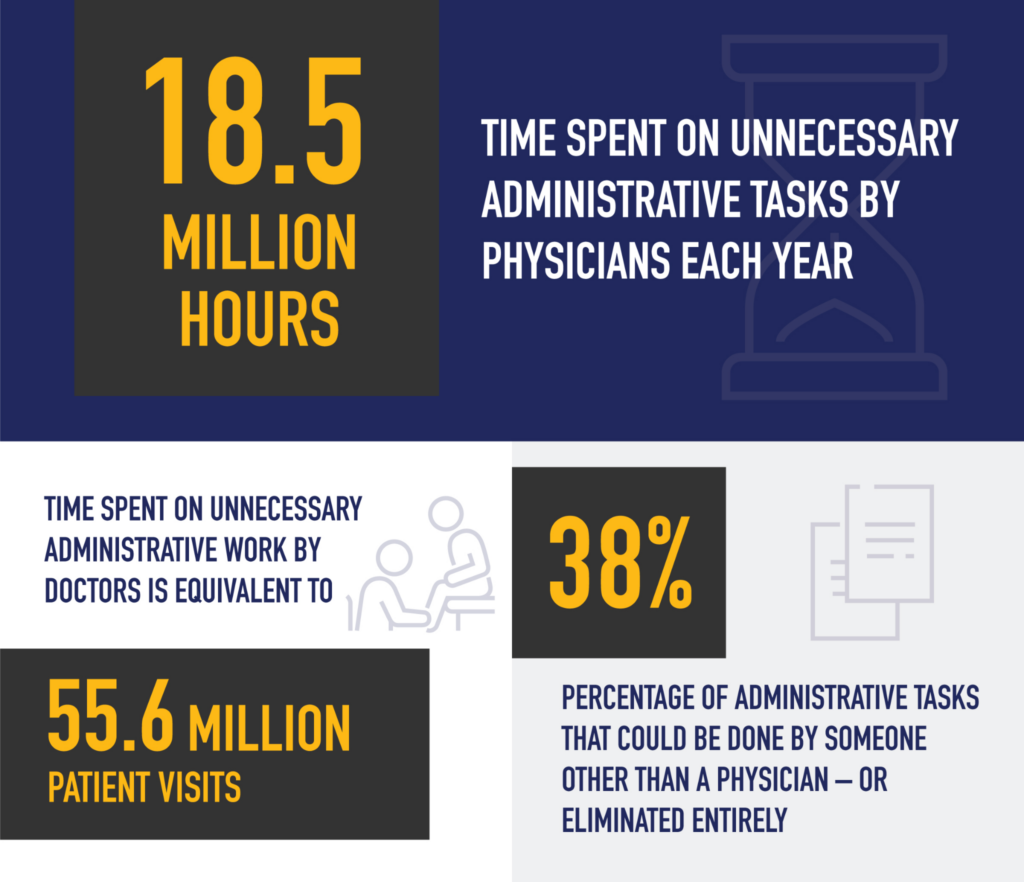

The numbers behind that volume are staggering. Canadian doctors spend an estimated 18.5 million hours each year on unnecessary paperwork and administrative tasks, hours that translate directly into 55.6 million missed patient visits annually.¹

The digitization of healthcare was supposed to help. Electronic Medical Records replaced paper charts. Automated faxing replaced manual routing. Ontario’s Health Report Manager was built to consolidate clinical communications. And yet, as LeBouthillier describes it, HRM created something worse than the paper era it replaced: *”In the past, with paper records, patients would go to emergency, they’d get admitted, they’d get all sorts of tests and at the very end, the primary care physician would get a discharge summary mailed to them that had everything in it.”*¹

Today, that same event generates an emergency room note, an admission notification, individual test updates, and a discharge summary, each arriving separately, each requiring a decision about whether action is needed right now. “It’s got a decision burnout effect on providers,” says LeBouthillier. *”You’re getting all this documentation and much of it is unnecessary because you can’t make any clinical decisions at that moment.”*¹

This is not a documentation problem. It is a data architecture problem, and it lives upstream of the clinical encounter, downstream of the patient outcome, and directly in the middle of every working day.

What a Real Practice Actually Looks Like to Run

Here is something medical school does not teach: running a clinic is running a small business. A practice with five physicians is managing payroll, vendor relationships, medical supply procurement, insurance verification, prior authorization pipelines, scheduling logic, billing reconciliation, and cash flow, simultaneously, every day, while also trying to deliver care.

“An estimated 25% of US healthcare spending goes toward administrative costs.” — Nitra Press Release, March 2026²

That figure, one dollar in four, gone before a patient is touched, represents the structural tax that inefficiency levies on the system. And unlike a startup burning cash on growth, there is no compounding return waiting at the end of that spend. It is pure friction. Lost time, lost margin, lost attention.

The back office of a medical practice typically runs on a patchwork of disconnected tools: a separate system for billing, a separate system for scheduling, another for procurement, another for payroll. Expense tracking happens in spreadsheets, or not at all. Supply orders go to multiple vendors at non-negotiated rates because no one has time to compare prices. A card gets compromised and it takes three days to figure out which vendor charged it.

As Nitra CEO Tim Hwang describes it: *”Practices are running critical workflows across disconnected systems that were never designed to work together.”*²

That is the real shape of the problem. Not one crisis. A thousand small disconnections.

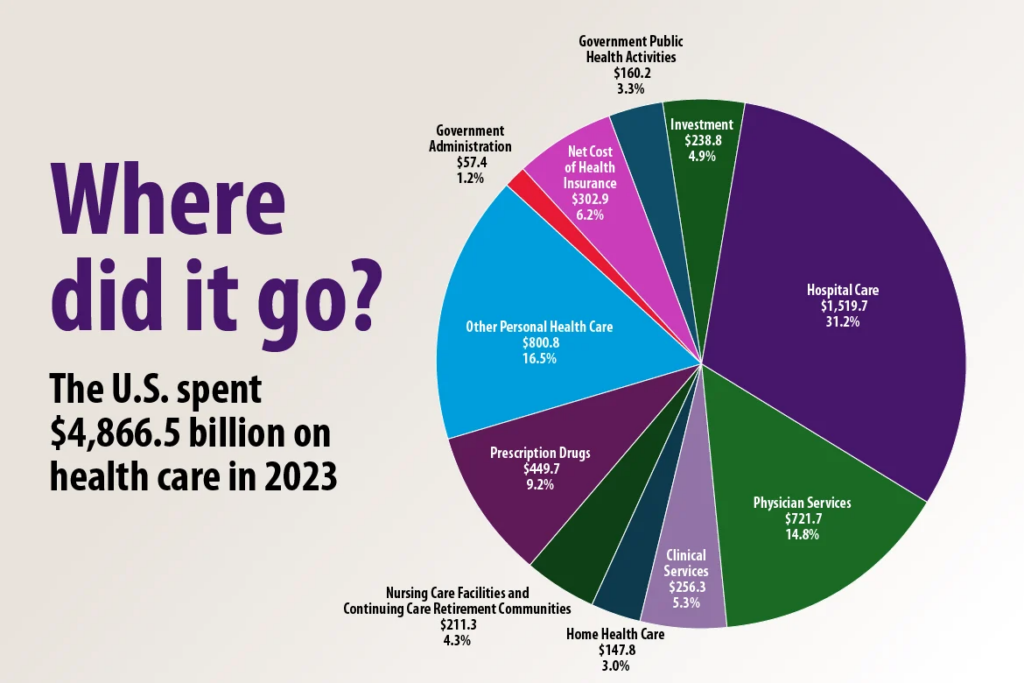

$4.8 Trillion. And a Quarter of It Disappeared Before Anyone Got Treated.

The United States spent $4,866.5 billion on healthcare in 2023. That number is large enough to be abstract, until you look at where it went.

Source: American Medical Association — U.S. National Health Expenditure Data 2023

Hospital care consumed the largest slice at $1,519.7 billion (31.2%). Physician services took $721.7 billion (14.8%). Prescription drugs: $449.7 billion (9.2%).

But here is the number that should stop any investor cold: government administration plus net cost of health insurance together account for roughly 7.4% of total spend, approximately $360 billion, before a single clinical decision is made. Add to that the estimated 25% of practice level spending consumed by administrative overhead that never appears cleanly in a national expenditure chart, and the picture becomes even starker.

The pie chart above shows where the money went. It does not show where the money was wasted. Those two things are not the same. Hidden inside the physician services slice, inside the hospital care slice, inside the clinical services slice, is an enormous volume of hours, staff time, and capital that went toward documentation, billing reconciliation, insurance verification, supply procurement, and prior authorization, not toward care.

McKinsey estimates AI could recover $200 – $360 billion annually from the US healthcare system through administrative efficiency gains alone, a figure that maps almost exactly onto the administrative overhead already embedded in that pie.

The market is not asking whether AI belongs in healthcare. It is asking which layer of the $4.8 trillion gets automated first, and who owns that infrastructure when it does.

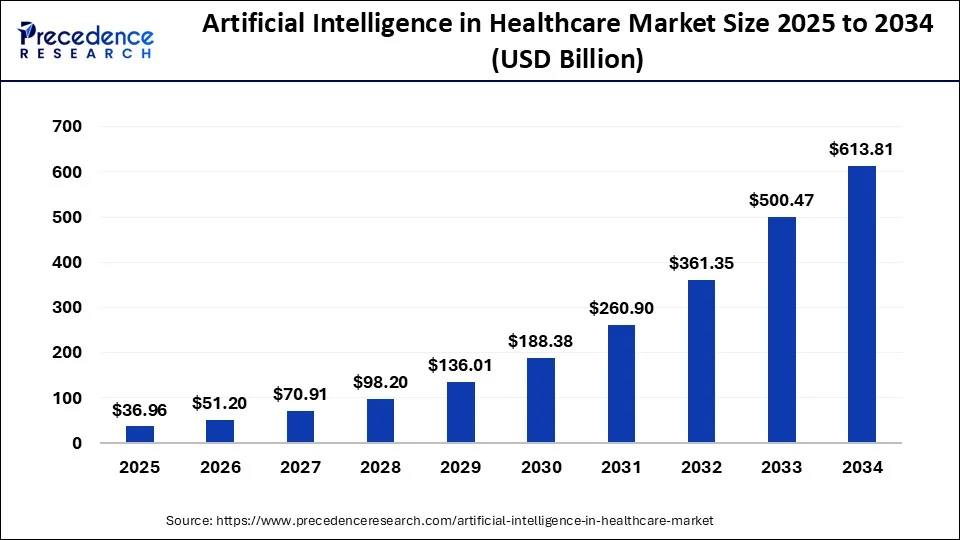

The Curve Nobody Is Debating Anymore

The AI in healthcare market was worth $36.96 billion in 2025. By 2034, Precedence Research projects it reaches $613.81 billion, a 17× expansion in under a decade.

Source: Precedence Research —precedenceresearch.com/artificial-intelligence-in-healthcare-market

Look at the shape of that curve. The first four years, 2025 to 2028, are relatively flat by comparison: $37B to $98B. Then the compounding hits. By 2030 the market has crossed $188B. By 2032, $361B. The acceleration in the back half of the decade is not a forecast anomaly, it is what technology adoption looks like when infrastructure catches up to demand.

This is the same shape semiconductors traced in the early 2000s. The same shape cloud computing traced in the early 2010s. The early years belong to the builders laying the plumbing. The back years belong to whoever owns the pipes.

Healthcare AI is still in the plumbing phase. The companies building the operational backbone of clinical practices today, the EMR layer, the workflow automation layer, the financial infrastructure layer, are not building for 2025 revenues. They are building for 2030 lock in.

The bar chart makes the timing plain. The window for early infrastructure ownership closes fast.

Three Companies Building the Fix

The market has noticed. AI enabled healthcare startups captured 62% of all US digital health venture funding in H1 2025, raising an average of $34.4M per round, an 83% premium over non-AI peers.³ The three most heavily funded sub-categories: non-clinical workflow automation, clinical workflow tools, and data infrastructure.³

These are not coincidences. They are the shape of where the real problem lives. Three early stage companies are building directly into the gaps.

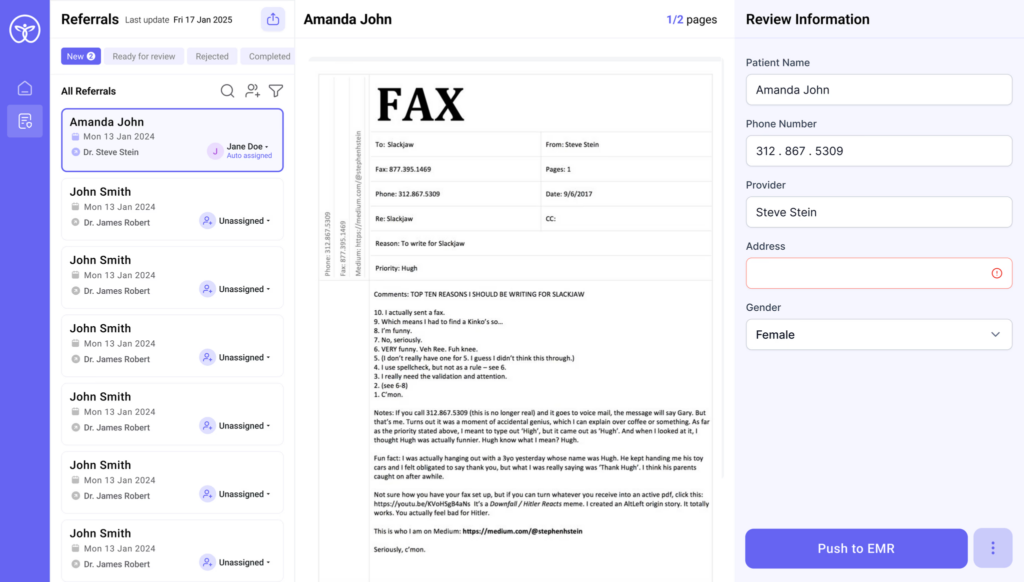

Company 01 — Ava Industries

Canada’s Award Winning EMR for Primary Care avaindustries.ca

From left to right Matt Henschke , MD CCFP, President, CVO, Director, Mike Forseth , MD CCFP, CEO, Director

The most fundamental layer of clinical infrastructure is the EMR, the system that captures what happens in the room. Ava Industries builds exactly this, but with a specific thesis: most EMRs were designed by engineers. Ava was designed by physicians.

The result is a platform that has earned a following not through marketing but through word of mouth from clinicians who are visibly relieved. “I just wanted to say how absolutely amazing Ava is. Literally I think I’ve lived longer because of it,” wrote Dr. Meyer, a physician user, in one of the company’s featured testimonials.⁴

What it solves. Ava’s core platform tackles charting, scheduling, eLabs integration, billing (both provincial and private), task management, and clinic management from a single screen. The philosophy is stated plainly on the product: two clicks to your task. The goal is not to add more features. It is to reduce the number of interactions required to accomplish any given workflow.

Ava AI, beyond scribing. Where Ava has moved furthest ahead is in its AI suite, which goes beyond the ambient scribe category to cover four distinct functions:

- Ava Scribe: Converts patient physician conversations into structured clinical notes in real time, directly inside the EMR, no plugins, no external integrations required.

- Document Classifier: Automatically sorts incoming faxes and eDeliveries with AI suggested labels, reducing the sorting burden that TELUS Health’s report identifies as one of the primary drivers of information overload.

- AutoChart: Reads visit notes and suggests structured chart entries in real time.

- Patient Care Plan: Generates personalized follow-up care plans post visit, helping close the loop on chronic condition management.

The Document Classifier deserves particular attention. Recall LeBouthillier’s description of the HRM problem: the physician receiving 12 pages of fragmented hospital updates when all they needed was the discharge summary. Ava AI’s classifier is built to solve exactly this, scanning incoming documents, identifying their type, and routing them appropriately without human triage.

Traction. Ava is trusted by over 2,200 providers and doctors, more than 8,000 clinical staff, and over 250,000 patient portal users.⁴ It serves 18+ Primary Care Networks (PCNs) across Alberta, British Columbia, and Ontario — giving it a provincial infrastructure footprint that early stage software companies rarely achieve.

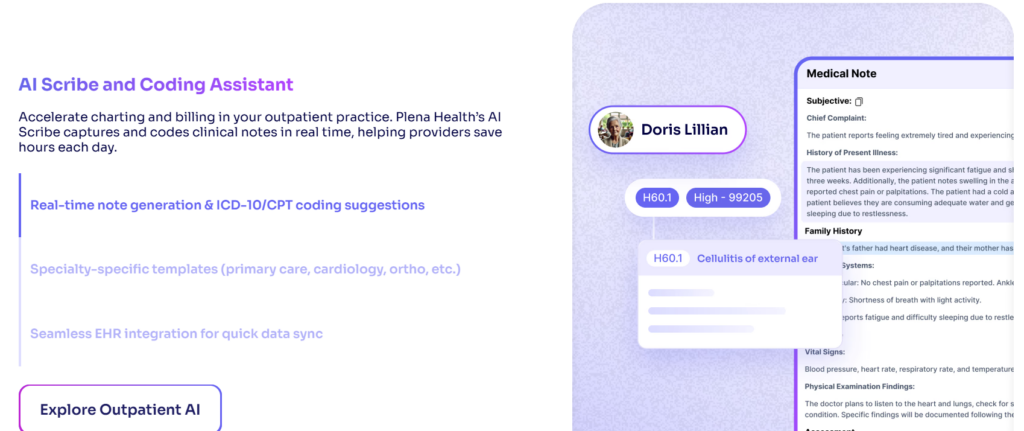

Company 02 — Plena Health

AI Workflow Automation for Clinical and RCM Operations plena.health

If Ava owns the clinical record layer, Plena Health owns the operational layer that wraps around it, the intake, scheduling, referral, billing, and front office workflows that determine whether a patient ever makes it into the room in the first place.

What it solves. Plena’s product suite operates across two distinct zones:

Pre-visit and front-office AI: Inbound referrals get converted from faxed or emailed documents into structured data automatically. Phone scheduling runs through an intelligent call routing system that books, triages, and manages appointments without staff involvement. Insurance eligibility checks happen instantly before appointments, preventing the last minute surprises that generate billing denials. Prior authorization requests, one of the most time-consuming workflows in any specialty practice, are automated end-to-end.

Clinical AI: Plena’s AI Scribe captures and codes clinical notes in real time, including ICD-10/CPT coding suggestions, meaning the documentation burden and the billing burden are addressed simultaneously, not sequentially. The system offers specialty specific templates across primary care, cardiology, orthopaedics, and more.

The integration thesis. What differentiates Plena is its emphasis on not disrupting existing infrastructure. The platform integrates with Epic, Cerner, athenahealth, and major billing platforms through flexible APIs designed to go live in weeks, not months. SOC 2 and HIPAA compliance are built in, not layered on after the fact.

Traction. Plena reports up to 80% less time spent on documentation, a 25% reduction in claim denials, and 100% improvement in provider satisfaction across its deployments.⁵ Integration timelines are measured in weeks. These are early stage metrics, but the directional signal matters: less documentation time, fewer billing errors, and staff who are no longer spending their days on tasks that don’t require a human.

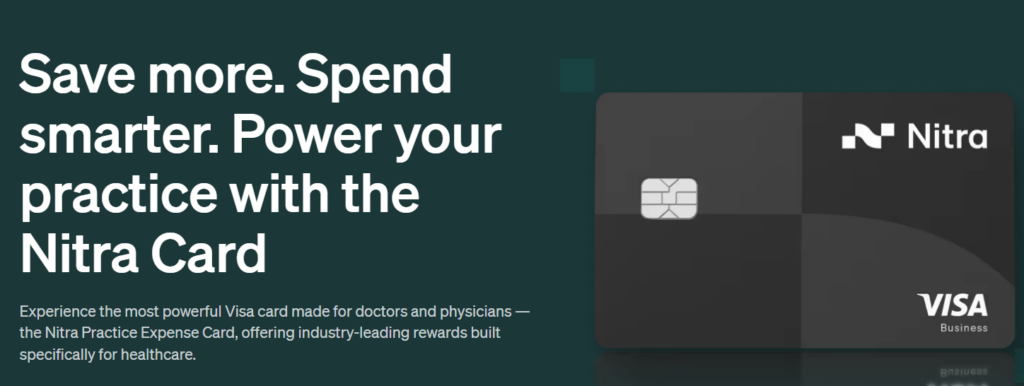

Company 03 — Nitra

The AI-Native Operating System for Healthcare Practice Back Offices nitra.com

From left: Tim Hwang, CEO; and Jonathan Chen, President.

If the first two companies solve the clinical and operational front-of-house, Nitra solves everything behind the curtain. It is, in the company’s own framing, an AI-native operating system for the practice back office, covering finance, procurement, inventory, and patient administration in a single platform.

The founding insight. Nitra was built by Tim Hwang and Jonathan Chen on a simple but underexplored observation: healthcare practices are small businesses, but no one has built the financial infrastructure to treat them that way. As Hwang puts it: *”Practices are running critical workflows across disconnected systems that were never designed to work together. Nitra brings those layers together into a single AI-native operating system.”*²

What it solves.

Financial automation: Nitra issues a Visa powered expense card with up to 2.2% cash back on medical and healthcare purchases, paired with AI powered accounting automation that codes transactions and flags anomalies in real time. Bill pay, expense analytics, virtual cards by vendor, and QuickBooks/Xero/Sage/NetSuite sync are all included. The system supports unlimited virtual cards, meaning each vendor gets its own card, so a compromised number or a vendor dispute can be isolated and resolved in minutes rather than days.

Commerce and inventory: NitraMart, the company’s integrated medical supply marketplace, gives practices access to tens of thousands of biopharma and medical equipment products from distributors including McKesson and Medline. AI procurement agents handle vendor onboarding, price negotiation, purchase execution, and inventory monitoring end-to-end. In December 2025 alone, Nitra supported upwards of $9 million in high stakes, patient critical biopharma purchases for physicians in a single day.²

Patient management: Launched in early 2026, Nitra’s voice AI agent automates patient scheduling and insurance eligibility verification, integrating with leading EHR systems including ModMed and Nextech.

Traction, and the numbers are hard to ignore. In 2025, Nitra grew revenues 740% — from $4M to over $33M in annualized revenue in a single year. The platform now serves 700+ healthcare practices and 2,500+ doctors and healthcare administrators, processing over $1 billion in annualized payment volume.²

In March 2026, Nitra raised $187 million in total financing across a Series B, venture debt, and a warehouse facility — bringing total capital raised to $205 million. The round included investors such as New Enterprise Associates (NEA), Andreessen Horowitz (earlier Seed round), and Pantera Capital. Dr. Richard Park, founder of CityMD (acquired for $8.9 billion by VillageMD), joined the board.²

The company is targeting 3,000+ clinics and $4 billion in annualized processing volume by the end of 2026.²

740% Nitra revenue growth in 2025

$1B+ Annualized processing volume

$187M Raised in March 2026 financing

The Stack, Mapped

These three companies are not competing. They are occupying adjacent layers of the same unsolved problem.

| Layer | Problem | Company |

| Clinical Record | Documentation, charting, note generation | Ava Industries |

| Operational Front-Office | Intake, referrals, scheduling, billing, prior auth | Plena Health |

| Practice Back Office | Finance, procurement, inventory, patient admin | Nitra |

Together, they represent a full-stack answer to what TELUS Health describes as the core challenge: *”I think about what we deal with every day: it’s information in, information out.”*¹ Ava handles the clinical information. Plena handles the operational information. Nitra handles the financial and procurement information.

The physician at the center of that system, Dr. Reyes, arriving at 7:42 AM to her inbox of 47 faxes, gets her time back. Not because medicine became easier. Because the systems around her finally started doing what systems are supposed to do.

What Could Slow This Down

EHR integration debt remains the central chokepoint. According to McKinsey’s Q4 2025 survey, 43% of healthcare leaders cite integration challenges as the top barrier to scaling AI, not risk, not regulation, not budget.⁶ Every one of these companies is building against that friction. All three emphasize fast integration timelines. The proof will be in how that holds at scale.

Regulatory environments differ across borders. Ava operates in a Canadian provincial healthcare context with distinct billing and data requirements. Nitra is primarily US focused. Plena bridges both. Navigating provincial and federal compliance frameworks, particularly as Canada’s proposed AI and data legislation develops, will shape how quickly these platforms can expand.

Adoption inertia inside practices is real. LeBouthillier’s advice, drawn from the TELUS Health report, is worth heeding: *”Providers can start by using AI for simple tasks like documentation and note-taking, and gradually move towards more complex tasks like automated scheduling or data analysis.”*¹ The best products in this space are not the ones with the most features. They are the ones that slot into existing workflows without demanding a behavioural overhaul from a physician who is already behind.

The AI divide is already forming. Deloitte’s 2026 survey found that among early AI adopters in healthcare, 59% expect cost savings above 20% in the next two to three years. Among organizations still watching: 13%.⁷ The gap will compound. Practices that invest in operational infrastructure now will be structurally cheaper to run, better staffed, and more financially healthy than those that don’t. This is not a technology story. It is a competitive moat story.

The Bottom Line

The challenge facing clinical medicine is not a shortage of smart people. It is a shortage of time, time that has been systematically consumed by information overload, disconnected back-office systems, and tools that were built for administrators rather than for the humans trying to provide care.

The companies that win in this space will not be the ones that build the flashiest AI. They will be the ones that disappear into the workflow, present enough to do the work, invisible enough to stay out of the way. Ava, Plena, and Nitra are three early bets on what that infrastructure looks like.

The market is open. The urgency is real. And somewhere, Dr. Reyes still has 44 faxes left to sort.

Sources

¹ TELUS Health: Artificial Intelligence and the Future of Healthcare — How Smart Automation Is Easing the Administrative Burden for Healthcare Practitioners

² Nitra: Nitra Raises $187 Million as AI-Native Platform for Healthcare Practices Surpasses $1 Billion in Processing Volume (March 10, 2026) https://www.nitra.com/resources/nitra-raises-187-million-as-ai-native-platform-for-healthcare-practices-surpasses-1-billion-in-processing-volume

³ Qubit Capital: AI in Healthcare: Investment Trends, Opportunities & Market Growth 2026 https://qubit.capital/blog/ai-healthcare-investment-trends

⁴ Ava Industries: Ava EMR — Canada’s Award Winning EMR for Primary Care and Clinics https://www.avaindustries.ca / https://www.avaindustries.ca/ava-ai

⁵ Plena Health: Plena Health AI Automation — Platform Overview https://www.plena.health

⁶ McKinsey: Generative AI in Healthcare: Adoption Matures as Agentic AI Emerges (April 2026) https://www.mckinsey.com/industries/healthcare/our-insights/generative-ai-in-healthcare-current-trends-and-future-outlook

⁷ Deloitte: Many Health Care Leaders Are Leaning Into Agentic AI as Adoption Hurdles Ease (February 2026) https://www.deloitte.com/us/en/insights/industry/health-care/agentic-ai-health-care-operating-model-change.html